Key takeaways

You may have multiple equity grants because of a promotion, a performance bonus, or standard company policy – or even because of a fall in your company’s valuation.

Multiple equity grants affect your overall vesting schedule, and they can be structured in either a parallel or serial format.

The strike price on subsequent grants is likely to be higher than your first grant.

Deepening your ties

Here’s some good news – your first equity grant at your company may not be your last equity grant.

It is possible (and in fact increasingly common) for startups to grant employees additional equity grants for various reasons. You could be two years into your employment and suddenly receive the pleasant surprise of a new stock option grant. It could be because of a promotion, for outstanding performance, or maybe even something you negotiated when you took the job.

But while these follow-on option grants (also known as option refresh grants or top-up option grants) are great, they could impact your vesting schedule, your exercise costs, and potentially even your career trajectory.

Managing overlapping vesting schedules

The standard vesting schedule for initial equity grants is typically four years with a one-year cliff. If you only have one equity grant, it makes it relatively easy to calculate how many shares you are vesting at one time and the cost to exercise (not including taxes).

But what happens when you receive a follow-on option grant? What vesting schedules are attached to these grants? There are two main ways companies can structure the vesting schedules of these follow-on grants – parallel and serial.

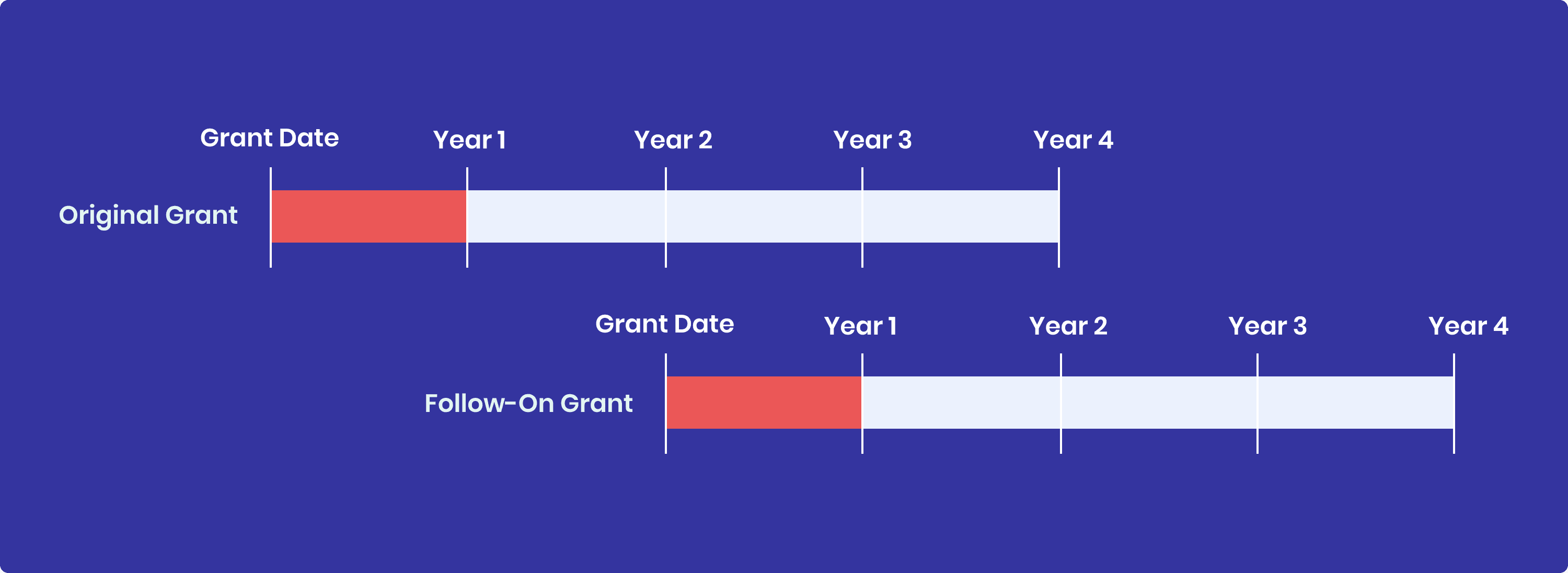

Parallel vesting schedules

In this structure, your follow-on grant would have its own vesting schedule that runs parallel to that of your original grant. For example, let’s say you received a “performance bonus” follow-on grant at the two-year mark with your company. And both your initial and follow-on grants have the same vesting schedule – four years with a one-year cliff.

As you can see, now all your options would only fully vest six years after the grant date of your original grant. It could be earlier or later, depending on when you received the follow-on grant. But the point is that in this structure, the vesting schedule of your follow-on grant is completely independent of your original.

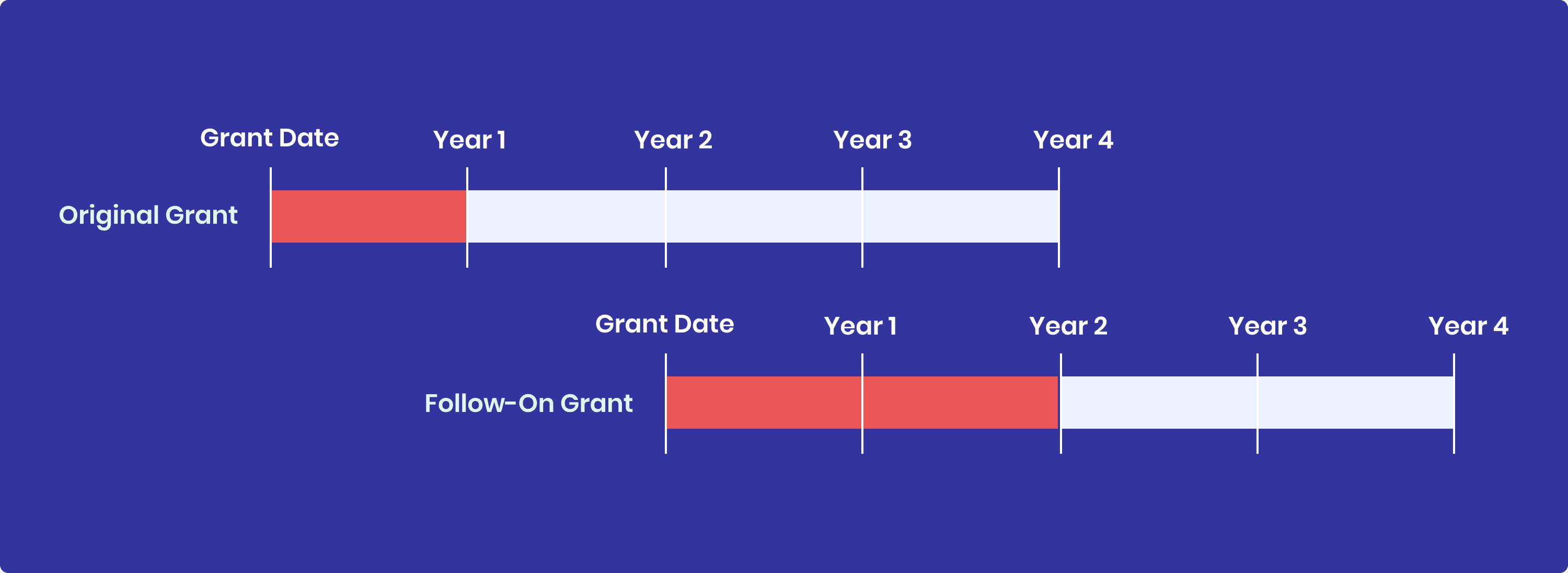

Serial vesting schedules

In this scenario, the vesting schedule of your follow-on grant is structured in a way that is “tacked on” to the end of your original one. This means the options in your follow-on grant would only begin vesting after all the options in your original grant had fully vested.

This structure is sometimes called a “boxcar” schedule, like train cars that keep getting added to the line. But what you should pay attention to is that it will extend the date that all your options vest significantly.

For instance, going back to the previous example, your company could add a two-year cliff to your follow-on grant. That way your follow-on grant will only start vesting at the end of year 4 – after your original grant has fully vested.

Two things to watch out for when you have multiple grants

While having multiple equity grants is a good thing, there are a few things to keep in mind.

1) Different strike prices

The strike price of your stock options grant will usually correspond with your company’s most recent 409A valuation. This means you'll likely have a higher strike price for the follow-on grant – and thus lower potential upside – compared to your original grant.

For instance, your original grant may have been 5,000 options at a strike price of $10/share. Your follow-on grant three years later may be 2,500 options – but this time at a strike price of $20/share. While the follow-on grant is ostensibly half your original grant, your potential upside is actually less than that. Keep this in mind when assessing the value of your follow-on grants.

👉 Your strike price for a subsequent grant is likely to be higher than your first equity grant. Remember, your strike price is what you pay per option when you exercise.

2) Golden handcuffs

Stock option grants can act as “golden handcuffs” that keep you tied to a company – even when opportunity calls elsewhere. You may end up telling yourself that you’re just waiting for all your options to vest before leaving. So, what happens when you’re given more options and it now takes two or three more years longer for all your options to vest?

There is no simple standard answer to this question. Sometimes, it may be worth staying. Other times, it might be worth just exercising your vested options and letting the unvested ones go.

👉 You need to calculate the opportunity cost and real cost of exercising additional equity grants.

This material has been prepared for informational purposes only and is not intended to provide, and should not be relied on for investment, tax, legal, accounting, or other professional advice. Vested does not provide investment, tax, legal, accounting, or other professional advice. You should consult your own investment, tax, legal, accounting, or other professional advisors before engaging in any transaction or equity decision.